Statement of Stephen C. Goss,

Chief Actuary

Social Security Administration

Testimony before the House Committee on Ways and Mean, Subcommittee on Social Security

March 22, 2016

Chairman Johnson, Ranking Member Becerra, and members of the subcommittee, thank you very much for the opportunity to speak to you today about the way Social Security benefits are adjusted currently for workers with earnings not covered under the program, and recent proposals to modify this adjustment. I will focus on the effects on Social Security beneficiaries of H.R. 711, introduced by Chairman Brady with Representative Neal on February 4, 2015, and the proposal included in the President's Fiscal Year 2017 Budget. Each of these proposals included modifications of the Windfall Elimination Provision (WEP) that applies to primary benefits for retired-worker and disabled-worker beneficiaries, as well as to auxiliary benefits for their spouses and children. Please refer to our enclosed letters providing estimates of the implications of these proposals for Social Security actuarial status, which are also available at https://www.ssa.gov/oact/solvency/index.html.

Present Law Windfall Elimination Provision (WEP)

Under current law, retired-worker and disabled-worker beneficiaries have their primary insurance amount (PIA) computed with a three-segment formula, which applies a 90 percent factor to the lowest portion of their average earnings, 32 percent to a substantial “middle” portion of their average earnings, and 15 percent to the highest portion of earnings for high earners. Average earnings are computed reflecting the highest 35 years of covered earnings for most retirees, and fewer years included for most disabled workers. Career-average covered earnings for workers who have some non-covered earnings are generally lower than career-average covered earnings for similar workers who worked solely in covered employment. Therefore, a higher proportion of average covered earnings are in the lower PIA formula bracket, and in turn, the PIA formula provides a higher “replacement rate,” (that is, the ratio of PIA to career-average indexed earnings) for these workers than for similar workers who worked solely in covered employment.

In order to offset the advantage, or windfall, provided in the PIA formula for workers with non-covered earnings, the WEP gradually reduces the 90 percent PIA factor used for beneficiaries with 30 or more years of substantial covered earnings to 40 percent for those with 20 or fewer years of substantial covered earnings.. A similar adjustment is applied for disabled worker beneficiaries with non-covered earnings.

The WEP is limited in application so that it does not reduce the PIA by more than one-half of the amount of the retirement or disability pension (periodic payment) received by the worker based on non-covered employment. Worker beneficiaries who are not known to be receiving periodic payments based on their non-covered earnings do not have their PIA reduced by the WEP.

Proposed Change in WEP for Worker Beneficiaries Newly Eligible in the Future

The proposal introduced by Chairman Brady and Representative Neal (H.R. 711) and the proposal included in the President’s Fiscal Year 2017 Budget would ultimately alter the adjustment of worker primary benefits in the same way, starting with those newly eligible for worker benefits in 2017 for H.R. 711 and in 2027 for the President's proposal. This new adjustment would effectively apply the benefit replacement rate the worker would have had if all of his or her earnings had been covered under the Social Security program, to the worker's average indexed monthly earnings (AIME) using only covered earnings on which payroll taxes were paid.

Adjusted PIA = ( PIA using all earnings / AIME using all earnings ) * AIME using covered earnings only

This adjustment would be applied whether or not the worker is eligible for or receiving a pension based on non-covered earnings, and does not include a limitation based directly on the number of years of substantial covered earnings (in other words, the 30-years-of-coverage exclusion is eliminated). Because the Social Security Administration has records of non-covered earnings for years after 1977, but does not have universal access to records for receipt of non-covered pensions, this new adjustment would be much easier to apply, and would be applied much more uniformly to all workers with some years of non-covered earnings.

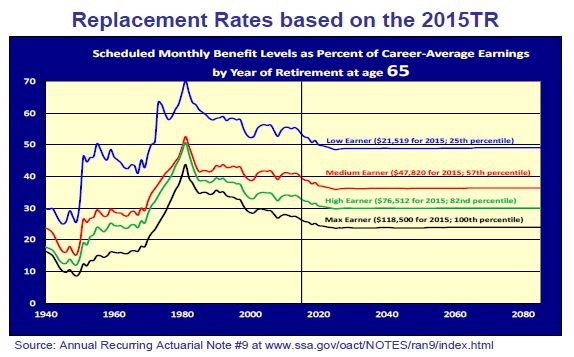

The figure below illustrates how the benefit replacement rate varies for retired-worker beneficiaries (retirees starting benefits at age 65) depending on the level of their career-average covered earnings.

For example, a worker with career-average earnings of $47,820, our “medium earner,” receives a retirement benefit of about 40 percent of their career-average earnings. However, if the same worker happens to have worked in non-covered employment for a little over half their career, such that their career-average covered earnings are only at $21,519, the level for our “low earner,” then the benefit will be about 53 percent of the career-average covered earnings. While the current WEP attempts to adjust for this disparity, the variability in pensions based on non-covered earnings and the reporting of these pensions leads to inconsistent adjustments in benefit levels.

The change proposed in H.R. 711 and in the Fiscal Year 2017 Budget makes a direct adjustment to the replacement rate such that the worker described above (overall career-average earnings at the medium-earner level, with a little over half of the earnings in non-covered employment, so that their career-average covered earnings would be at the low–earner level) would receive a benefit replacement rate of 40 percent, instead of 53 percent. This adjustment would occur uniformly and consistently for individuals with split careers between covered and non-covered earnings. Differences in pension levels and reporting by various non-covered employers would no longer influence the adjustment to Social Security worker benefits. The implicit rationale for this approach may be characterized as: for years of non-covered earnings, where neither the employer nor the employee paid Social Security payroll tax, the employee and employer should be responsible for providing pension coverage and disability protection.

Ultimate Effects on Beneficiaries of the New WEP Adjustment

In order to meaningfully illustrate the effects of the new adjustment on workers who will become eligible starting in 2017 and 2027, respectively, under these proposals, we provide estimates of the effects of the new adjustments on all current beneficiaries in 2016, as though the new approach applied to them. The average monthly WEP reduction for workers in 2016 with the current approach is about $270.

For the roughly 1.5 million retired-worker and disabled-worker beneficiaries in 2016 whose primary benefit is reduced under the current WEP, the new adjustment would result in an increased primary benefit for about 1.25 million beneficiaries (about 84 percent of all currently-affected beneficiaries). The average reduction would be about $77 less on average, from $274 per month under the current WEP to about $198 per month under the new adjustment. The remaining 0.25 million beneficiaries (about 16 percent of all currently-affected beneficiaries) would see a further small reduction in their primary benefit. Their average reduction would be about $13 more on average, from $190 per month under the current WEP to about $203 per month under the new adjustment.

For 2016, we estimate that there are roughly 15 million retired-worker and disabled-worker beneficiaries with some non-covered earnings after 1977 who are not reduced under the current WEP. We estimate that for about 1 million (about 7 percent) of these beneficiaries, the new adjustment (if it were in place in 2016) would not change their primary benefit. For the other 14 million beneficiaries, the average reduction in benefit would be about $27 per month for 2016. For the half of this 15 million least affected by the new adjustment, the average primary benefit reduction would be just $3 per month. For the half most affected, the reduction would average $46 per month. About 55 percent of the 15 million, or roughly 8 million beneficiaries, qualify for exemption from the current WEP because they have 30 or more years of substantial covered earnings. Because these 8 million retired-worker or disabled-worker beneficiaries have relatively few years of non-covered earnings, their reduction under the new approach would be relatively small. In addition, more than 75 percent of these 15 million workers have fewer than 5 years with any non-covered earnings.

Proposed Change in WEP for Worker Beneficiaries Newly Eligible in the Past or Near Future

Both proposals would expand the application of the current WEP to worker beneficiaries first eligible before the implementation of the new adjustment formula.

Under H.R. 711, all individuals eligible for retired-worker or disabled-worker benefits for December 2016 who: (1) have any recorded non-covered earnings after 1977, (2) are not currently affected by the WEP, and (3) have less than 30 years of substantial covered earnings, would be required to obtain by the end of 2016 certification from any employer who paid him or her non-covered earnings. This certification would indicate whether the worker is vested for a pension, and when and how much pension has been received. A WEP reduction would be applied if it is determined to be warranted for past or future benefits. If the WEP reduction is applicable for past benefits, an overpayment would be established to be repaid by the beneficiary, principally through recovery from his or her future benefits. If an individual does not obtain certification, then the WEP would be applied for past and future benefits limited only by the number of substantial years of covered earnings.

Under H.R. 711, a “rebate” would be applied for all benefits reduced by the current WEP based on entitlement for months in 2017 and later. The rebate would be determined to be as high as possible, but not in excess of 50 percent of the WEP reduction, and limited to assure that the net effect of the Bill on Social Security program cost through 2025 would be neutral or positive. We estimate that the maximum permissible rebate percentage of 50 percent would be applicable.

Under the President's proposal in the 2017 Budget, employers would be required to report all periodic payments (pensions) based on non-covered earnings for past and future years, for workers who were or will be first eligible for a retired-worker or disabled-worker benefit before 2027. This additional reporting, particularly from state and local governments, will lead to additional workers being subject to WEP reduction for past and future benefits.

Effects on Beneficiaries of the Increased Application of the Current WEP

Under H.R. 711, we estimate that up to 10 percent of the 7 million worker beneficiaries in December 2016 with some past non-covered earnings, fewer than 30 years of substantial covered earnings, and no current WEP reduction would be determined to warrant a WEP reduction on some past or future benefits. This assumption is very uncertain, and the actual number would depend substantially on the efforts made by beneficiaries and their former employers to produce and obtain valid certification of their pension vesting and payments received. We estimate that for this group, the average amount of overpayment made before 2017 that would be recovered in 2017 through 2025 will be roughly $8,000. For future benefits to this group, the average total benefit reduction through 2025, net of the 50-percent rebate, will also be roughly $8,000. Recovery of overpayments for prior months would be limited by the financial status of the beneficiaries and the remaining duration of their benefit receipt. Thus, the number of individuals with recovery and reduction of benefits is very uncertain.

Under the President's proposal, we estimate that establishing systems for reporting of pension payments based on non-covered earnings would require about 3 to 6 years to fully develop and would ultimately capture most but not all non-covered pension recipients. We estimate that the percentage of the 7 million worker beneficiaries in December 2016 with past non-covered earnings, fewer than 30 years of substantial covered earnings, and no current WEP reduction who would be determined to warrant a WEP reduction on some past or future benefits under the President’s proposal would be significantly lower than for the process under H.R. 711. In addition, because reductions and recoveries would be applied only for months with verified receipt of pension payments and would be limited based on the size of the pension payments, the average reduction or recovery might be smaller per month than under H.R. 711. Overall, we estimate that program savings through 2025 for benefit reductions and recoveries under the President’s proposal for worker beneficiaries entitled for December 2016 would be less than half the amount expected under the provisions of H.R. 711. Under the President’s proposal, however, additional workers becoming newly eligible for retired-worker or disabled-worker benefits after December 2016, through 2026, would also be found to have non-covered pension payments requiring application of the WEP adjustment.

Government Pension Offset (GPO)

The President's proposal would utilize the additional reported pension data to improve application of the current law GPO. The proposal would also change the GPO provision for those eligible after 2026, limiting the offset to spouse benefits (including divorced and surviving spouses) at age 62 or older and to spouse benefits for those also receiving any Social Security benefit based on their own disability (including disabled worker, disabled widow, and disabled adult child beneficiaries under age 62). The offset would be applied to these auxiliary benefits more consistently, based on their past earnings in non-covered employment. The new offset would reduce the amount of the auxiliary benefit by the excess of (1) the auxiliary beneficiary's own potential retired-worker or disabled-worker benefit based on all of his or her earnings over (2) the auxiliary beneficiary’s potential worker benefit based on covered earnings only. This excess amount would be calculated and applied regardless of the insured status of the auxiliary beneficiary. This provision contributes to the program savings under the President's proposal as indicated in our letter to the Director of OMB. It is our understanding that the intent of this hearing is to explore proposals affecting the WEP adjustments on primary benefits for workers, so I will not cover the details of the GPO provisions in this testimony.

Conclusion

Both H.R. 711 and the President's proposal in the Fiscal Year 2017 Budget would ultimately result in a more consistent and logical adjustment to the primary benefit amounts for workers with career earnings split between covered and non-covered employment. The analysis offered here reflects intense analytical work by several people in our office, but particularly Jacqueline Walsh and Bert Kestenbaum (now retired). We appreciate the opportunity to share the results of our analysis and our estimates for the effects of these proposals. They are, as always, a work in progress. I will be happy to attempt to answer any questions you may have.

Stephen C. Goss response to Chairmen Brady

Stephen C. Goss response to OMB Director Donovan

_________________________________________________________________________________________________________________________________________________________

Statement for the Record of Samara Richardson,

Acting Associate Commissioner, Office of Income Security Programs

Social Security Administration

Testimony before the House Committee on Ways and Mean, Subcommittee on Social Security

Chairman Johnson, Ranking Member Becerra, and Members of the Subcommittee:

Thank you for the opportunity to discuss Social Security coverage and how we compute benefits for individuals who worked part or all of their careers in non-covered employment where they did not pay Social Security taxes (“non-covered work”). My name is Samara Richardson, and I am the Social Security Administration’s (SSA) Acting Associate Commissioner for the Office of Income Security Programs. My testimony today will:

• summarize the history of Social Security coverage;

• describe the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO);

• provide an overview of issues with WEP and GPO and describe how we administer them; and

• discuss the Administration’s legislative proposal, which would simplify and improve administration of WEP and GPO.

Importance of Social Security

Before discussing the topic at hand, I would like to describe briefly the Old-Age, Survivors, and Disability Insurance (OASDI) (or “Social Security”) program. Social Security is a social insurance program, under which workers earn coverage for retirement, survivors, and disability benefits by working and paying Social Security taxes on their earnings.

Few government agencies touch as many people as we do. Social Security pays monthly benefits to more than 59 million individuals, consisting of 40 million retired workers and 3 million of their spouses and children; 9 million disabled workers and 2 million dependents; and 6 million surviving widows, children, and other dependents of deceased workers. Last year, these benefits totaled around $880 billion. Administrative costs are very low, at less than 1 percent of benefit payments. The Fiscal Year 2017 President’s Budget for SSA will allow us to tackle our hearings backlog, improve overall service, and save billions of taxpayer dollars through increased program integrity work.

Social Security Coverage

When a job is covered by Social Security, the Social Security tax rate for wages paid (up to an annual limit)1 is set by law at 6.2 percent for employees and employers, each.2 After paying Social Security taxes over a sufficient period, a worker becomes insured for Social Security benefits. Workers become eligible to receive retirement benefits beginning at age 62 or may receive disability benefits at earlier ages if other criteria are met. Workers also earn Social Security protection for their family members; for instance, the spouse of a worker may receive spousal benefits if the worker is receiving retirement or disability benefits. As discussed more fully below, spousal benefits will be reduced if the spouse is also eligible to receive retirement benefits based on his or her own work.

When Congress enacted the Social Security Act in 1935, fewer than 50 percent of the nation’s workers were covered. But over time, Congress has expanded coverage to most jobs, and today it is nearly universal—about 96 percent of the nation’s workforce is currently covered by Social Security and paying Social Security taxes.

Most of the 4 percent of workers not covered by Social Security are State and local government employees who earn alternative pensions. Today about 28 percent of State and local workers are not covered by Social Security. Other non-covered employees include certain employees of railroads, non-profit organizations, and the Federal government hired before 1984. These employees do not pay Social Security taxes on their non-covered earnings and earnings from these jobs are considered non-covered for purposes of the Social Security benefit calculation.

History of Coverage

In 1950, Congress enacted legislation that allowed States to enter into voluntary agreements to provide Social Security coverage to State and local employees not covered under a retirement system. After the 1950 legislation, Congress enacted a number of other changes that expanded coverage of government employees, including:

• The 1954 amendments made coverage available to State and local employees covered under a retirement system, at the election of the employer and employees;

• In the 1983 amendments, Congress repealed a provision allowing States to rescind agreements extending voluntary coverage to State and local employees, and required Social Security coverage for Federal, railroad, and nonprofit employees hired in or after 1984; and

• Legislation in 1990 made Social Security coverage mandatory for State and local employees who are not under a retirement system.

Social Security Benefit Formula

Under the Social Security Act, the formula used to calculate Social Security benefits is progressive: that is, it is weighted so that people who spend their careers in low-paying or intermittent jobs receive a benefit that is higher as a share of their average prior earnings than the benefit provided to people with high career earnings. Appendix A provides the formula used to calculate a worker’s primary insurance amount (PIA), which is based on a worker’s average indexed monthly earnings (AIME); the PIA forms the basis of the worker’s and his or her dependents’ benefits.

This formula “counts” only covered earnings. So, a person who has only non-covered earnings in a year is considered to have no earnings in that year. As a result, a person who spent most of his or her career in employment not covered by Social Security but had some covered work would appear to have low career earnings, and would be eligible for the higher benefit the weighted formula provides. This higher Social Security benefit, when combined with a government pension, would result in this person receiving a “windfall” as compared to those who had either only non-covered (and thus was ineligible for Social Security) or only covered work (and whose benefits are computed on a full accounting of their earnings. The Windfall Elimination Provision, described in the next section, is designed to eliminate this windfall and ensure that those with a combination of covered and non-covered earnings are not treated better under the Social Security formula than other workers.

Non-covered Earnings and the Windfall Elimination Provision

An individual’s career may include some jobs that were covered by Social Security and some that were not covered. They may be eligible for Social Security benefits based on their covered work as well as for pension benefits based on their non-covered work. The Social Security program did not initially adjust the benefits of individuals who received pension benefits for non-covered work. Before provisions were put in place to address this windfall, individuals with non-covered work may have received combined Social Security and government benefits that far exceeded those of other individuals, with identical lifetime income, who worked solely in either covered or non-covered work. Because not all of their lifetime earnings are counted for Social Security purposes, people with considerable non-covered earnings may appear to have spent their careers in low-paying or intermittent jobs, and so – because of the progressive benefit formula – would receive a relatively higher Social Security benefit than similar individuals who worked only in covered employment.

Congress recognized this inequity and enacted the Windfall Elimination Provision (WEP) under the Social Security Amendments of 19833 to correct it. The WEP reduces a worker’s retirement or disability benefits if such worker is also receiving a pension based on non-covered work.

Prior to the Social Security Amendments of 1983, the Report of the National Commission on Social Security Reform (informally known as the Greenspan Commission) recommended two potential ways to address this scenario.4 One approach would have modified the benefit formula as follows:

[A]pply the present benefit formula to an earnings record which combines both covered earnings and also non-covered earnings in the future for the purpose of determining a replacement rate (i.e., the ratio of the benefit initially payable to previous earnings); then, that replacement rate would be applied to the average earnings based solely on covered employment.

At that time, SSA did not have information on non-covered work in its records. SSA first began receiving non-covered earnings records in 1978. Without this data, Congress instead enacted the benefit reduction formula that is in the law today. Specifically, the WEP formula reduces benefits for individuals who receive a pension because of their non-covered work, on a sliding scale based on the number of years the person worked in covered employment. Appendix B shows how WEP affects the primary insurance amount (PIA). In 2016, the WEP reduces monthly retirement and disability benefits by a maximum of $428.00 per month. Applying WEP never eliminates an individual’s Social Security benefit completely.

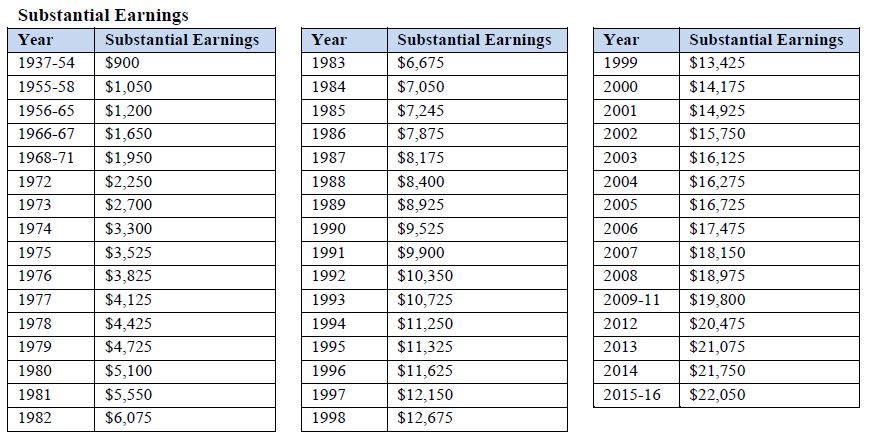

There are several exceptions to the WEP. The WEP does not apply to people who have 30 or more years of substantial5 covered earnings, and it is gradually reduced for workers who have 21 to 29 years of substantial covered earnings. In addition, the WEP does not affect beneficiaries who are not yet receiving pensions based on their non-covered earnings. Finally, the WEP can never reduce benefits by more than one-half the amount of the beneficiary’s pension, which protects individuals who receive relatively low pension amounts.

As of December 2015, the WEP reduced benefits for around 1,692,000 retired and disabled workers and their dependents. The majority of primary beneficiaries whose benefits are reduced by the WEP (99 percent) received benefits based on retirement.

Spousal (and Widow’s/Widower’s Benefits)& the Government Pension Offset

The spouses of workers receiving Social Security benefits may be eligible for spousal benefits. The spousal benefit is equal to 50% of the retired or disabled worker’s benefit and 100% of the deceased worker’s benefit. Individuals who qualify for both a Social Security worker benefit (retirement or disability) based on their own work history and a Social Security spousal benefit based on their spouse’s work history are “dually-entitled” and are subject to the dual-entitlement rule, meaning that their spousal benefit is paid only to the extent it exceeds their own retirement benefit. Individuals who qualify for both a non-Social Security-covered government pension and a Social Security spousal benefit are subject to the Government Pension Offset (GPO) provision. The intent of the GPO is the same as that of the dual entitlement rule: to reduce the Social Security spousal benefits of individuals who are not financially dependent on their spouse because they receive their own benefits. The key difference is what is used to determine financial dependence — benefits based on Social Security-covered work or benefits based on non-Social Security-covered work.

Dual-entitlement rule. The Social Security dual-entitlement rule requires that 100% of a Social Security retirement or disability benefit earned as a worker (based on one’s own Social Security-covered earnings) be subtracted from any Social Security spousal benefit one is eligible to receive (based on their spouse’s Social Security-covered earnings), and only the difference, if any, is paid as a spousal benefit. The Social Security spousal benefit of a person who receives a pension from government employment (federal, state, or local) that was based on work not covered by Social Security is reduced by a provision in the law known as the GPO, enacted in 1977.6

The GPO is intended to place annuitants whose government employment was not covered by Social Security and who are eligible for a Social Security spousal benefit in approximately the same position as workers whose jobs were covered by Social Security and are also eligible for a Social Security spousal benefit. Because SSA has not had complete earnings records of those who work in non-Social Security-covered positions, SSA has been forced to rely on the government pension as a measure of those uncovered earnings. Essentially, it is assumed that two-thirds of the government pension is equivalent to the Social Security retirement or disability benefit the spouse would have earned as a worker if his or her job had been covered by Social Security. Thus, the GPO attempts to replicate the Social Security dual-entitlement rule by requiring that an amount equal to two-thirds of the worker’s non-covered government pension be subtracted from the Social Security spousal benefit.

The GPO also has a variety of complicating exceptions. The Social Security Protection Act of 2004 (P.L. 108-203) amended the GPO provisions to require that State and local government employees covered by Social Security throughout their last 60 months of employment be exempt from GPO. Prior to this legislation, GPO did not apply if an individual’s last day of employment was in a position that was covered by both Social Security and a State or local government pension system. The “last day” exemption may still apply if the last day of employment was before July 1, 2004, or if the person filed for a Social Security spouse’s benefits before April 1, 2004, and was entitled to those benefits based on that filing. Additionally, the GPO does not apply to individuals who had filed for and were entitled to spouses benefits prior to December 1977.

As of December 2015, the GPO reduced benefits for around 652,000 spouses.

Issues with Current-Law WEP and GPO

While both WEP and GPO address inequities that existed prior to their enactment, there is room for improvement. Both provisions are difficult to administer and challenging for the public to incorporate into their retirement plans.

Issues of Administration

Social Security benefit payments are highly accurate; over 99 percent of the benefit dollars we pay are free of either an overpayment or underpayment. However, the WEP and GPO provisions are complex and time-consuming to administer and applying WEP and GPO remains a significant cause of improper payments in the OASDI programs.

To a large extent, this is because we do not have an automated way to access State and local pension information. Instead, we must rely primarily on beneficiaries to self-report when they receive a pension based on non-covered employment.

When a beneficiary does report receiving a pension based on non-covered work, our field office and program service center staff must develop, verify, and document relevant information, including when the person first became eligible for the pension, the monthly amount, and when the pension stops. This often involves contacting the pension-paying organization. In addition, for certain non-covered employees in nonprofits, administration may be further complicated because the organizations themselves may no longer exist or retain older records. Our staff must also determine whether any of the WEP or GPO exceptions apply.

For federal pensions, we exchange information with the Office of Personnel Management (OPM) to identify Social Security beneficiaries who are receiving a pension based on non-covered, Federal employment. We do not currently have similar exchanges with State and local governments.

Issues of Retirement Planning

We help people plan for retirement by making the Social Security Statement (“Statement”) available to every worker by mail or through a my Social Security account. The Statement informs each individual of the amount of benefits he or she can expect to receive at retirement age or upon becoming permanently disabled. These amounts do not reflect application of the WEP or GPO because we lack information in our records about the person’s non-covered pension status. Consequently, as required by the Social Security Protection Act of 2004, every Statement includes a disclaimer indicating that benefits may be lower than stated if the person were to receive a pension based on non-covered work. Individuals subject to WEP or GPO are often surprised when their benefits are less than expected.

Other Issues

We must rely on those who worked in non-covered employment including former State or local workers to report these pensions to us. However, because we have access to OPM’s information concerning Federal pensions based on non-covered work, we are much more likely to discover a Federal than a non-Federal pension. As a result, Federal workers are much more likely to be subject to the WEP and the GPO.

Finally, while we reduce a Social Security spousal benefit on a dollar-for-dollar basis by the amount of the person’s own Social Security retirement or disability benefit, under GPO, we reduce the Social Security spousal benefit by only two-thirds of the person’s pension based on non-covered work.

The Administration’s Proposal for the Fiscal Year 2017 Budget

The President’s Budget for Fiscal Year 2017 includes a legislative proposal that would improve the administration and fairness of the WEP and GPO provisions in several ways. First, it would eliminate our reliance on self-reporting by requiring State and local government pension providers to provide SSA with data on pensions based on non-covered, State and local employment. The proposal would also provide $70 million to establish these data exchanges, with up to $50 million of those funds dedicated to the States’ costs. We will use these data exchanges to help us administer WEP and GPO for current beneficiaries and individuals eligible for benefits prior to 2027. This change would build our capacity to identify State and local government retirees receiving pensions based on non-covered work. It would strengthen payment accuracy and provide equal treatment between Federal and non-Federal government workers.7

In addition, the Budget proposes to replace the current WEP and GPO for individuals who become eligible for benefits in 2027 or later. From that point forward, we would adjust benefits based directly on the worker’s total earnings record, without regard to whether he or she receives a pension based on those earnings. Consequently, this would ensure that persons with both non-covered and covered earnings are not treated more favorably than persons who solely worked in jobs for which they paid Social Security taxes.

We have collected and maintained information on non-covered earnings in our records since 1978. By 2027, we will have nearly 50 years of data on non-covered employment, which will allow us to calculate the amount by which benefits should be reduced without relying on either the applicant or the pension provider.

To carry out the proposed calculation that would replace WEP:

(1) We would calculate a combined Average Indexed Monthly Earnings (AIME)8 that includes any years of covered and non-covered earnings in a worker’s highest 35 years of earnings.

(2) We would then calculate a new “combined” PIA from this combined AIME. This amount is the equivalent Social Security retired worker benefit that the individual would have received had all of their work been in covered employment.

(3) We would divide the combined PIA by the combined AIME to determine, as the Greenspan Commission recommended for WEP in 1983, a replacement rate based on the average covered and non-covered earnings.

(4) We would then apply that replacement rate to the AIME based solely on covered employment to derive the actual PIA.

Additionally, the President’s Budget proposal would similarly modify the GPO. As with the new calculation to deal with a worker’s non-covered earnings, we would calculate a new AIME that includes any years of non-covered earnings. We would then calculate a new “combined” PIA from this new AIME. This amount is the equivalent Social Security retired worker benefit that the individual would have received had all of their work been in covered employment.

As under current law spousal benefits, this new retired worker benefit would be subtracted dollar for dollar from the spousal benefit the non-covered worker would be eligible for and only the difference, if any, would be provided as a Social Security spousal benefit.

Spouse's Covered and Noncovered PIA - Spouse's Covered PIA = New GPO Reduction

Appendix C includes examples of the proposed new computations for noncovered work. As the examples show, some individuals would receive more benefits than they would expect under current law, while others could expect to receive less. As with any policy change as significant as this one, it is critical to allow sufficient lead-time so that affected individuals can incorporate the change in their financial planning and decision-making. We believe that an effective date of 2027 allows enough time for individuals to adjust their retirement plans.

Conclusion

Congress created the WEP and GPO provisions so that Social Security benefits would remain progressive and fairly reflect an individual’s covered and non-covered earnings. However, in the absence of non-covered earnings data on which to calculate an appropriate benefit reduction, Congress based its reductions on the receipt of a non-covered pension. This approach was the most manageable solution, given the limited earnings information available for use in the late 1970s and early 1980s. However, we will soon have more than 40 years of non-covered earnings data in our records. These data will give us the capability to transition toward an alternative WEP and GPO formula based on these earnings. The Administration recommends such an approach, as it would simplify administration, reduce improper payments, and provide all workers with more equitable treatment. In the interim, the President’s Budget proposes requiring State and local government pension payers to provide us with non-covered pension data, thereby enabling us to apply current-law WEP and GPO more consistently and correctly.

We appreciate Chairman Brady’s leadership on this issue and his interest in, and efforts toward, a similar solution through his introduced bill, H.R. 711, the Equal Treatment of Public Servants Act of 2015. While there are a number of differences between the President’s and the Chairman’s proposed legislation, we would like to note their shared formula to replace the WEP.

This concludes my testimony. I appreciate the opportunity to appear before you today and would be happy to answer any questions you may have.

________________________________

1 In 2016, the amount of wages subject to OASDI taxes is $118,500.

2 Self-employed income is subject to an OASDI tax rate of 12.4, up to the annual limit.

3 Public Law 98-21, 97 Stat. 65.

4 See Report of the National Commission on Social Security Reform, https://www.ssa.gov/history/reports/gspan.html.

5 The amount of earnings considered substantial for WEP purposes is $22,050 in 2016. This amount is updated annually to account for inflation.

6 Public Law 95-216, 91 Stat. 1509.

7 As I noted earlier in my testimony, we currently have a data exchange with OPM to identify individuals who receive a Federal pension based on non-covered work.

8 The AIME is, in short, a person’s average monthly wages, calculated using his or her 35 highest years of earnings, and indexed for inflation. Please see Appendix A for more information.

___________________________________________________________________________________________________________________________________________________________

APPENDICES TO THE STATEMENT FOR THE RECORD

Appendix A: Determining Primary Insurance Amount

PIA Definition

The “primary insurance amount” (PIA) is the benefit a person would receive if he or she elects to begin receiving retirement benefits at his or her normal retirement age. At this age, the benefit is neither reduced for early retirement nor increased for delayed retirement.

PIA Formula Bend Points

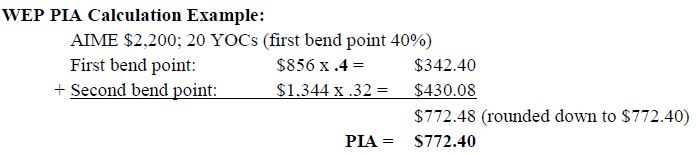

The PIA is based on a person’s average indexed monthly earnings (AIME). The PIA is the sum of three separate percentages of portions of a person’s AIME. The portions depend on the year in which a worker attains age 62, becomes disabled before age 62, or dies before attaining age 62.

For 2016, these portions are:

the first $856 of AIME,

the amount of AIME between $856 and $5,157, and

the amount of AIME over $5,157.

These dollar amounts are the “bend points” of the 2016 PIA formula. The table at the following link shows bend points for years beginning with 1979: ://www.ssa.gov/oact/cola/bendpoints.

PIA Formula

For an individual who first becomes eligible for old-age insurance benefits or disability insurance benefits in 2016, or who dies in 2016 before becoming eligible for benefits, his or her PIA will be the sum of:

90 percent of the first $856 of AIME

+ 32 percent of AIME over $856 and through $5,157

+ 15 percent of AIME over $5,157

We round this amount to the next lower multiple of $.10 if it is not already a multiple of $.10.

PIA Calculation Example:

___________________________________________________________________________________________________________________________________________________________

Appendix B

Windfall Elimination Provision (WEP)—(Current Law)

Under the WEP, we will reduce a worker’s retirement or disability benefit if the worker has fewer than 30 years of “substantial earnings.” Specifically, for those who reach 62 or became disabled in 1990 or later, we reduce the first bend point (the 90 percent factor in our formula) to as little as 40 percent. The bend point reduction depends upon the worker’s number of Years of Coverage ($22,050 of covered earnings in 2016).

WEP Guarantee (or Minimum): The law protects a worker who receives a low pension. We may not reduce a Social Security benefit by more than half of the worker’s noncovered pension.

__________________________________________________________________________________________________________________________________________________________

NEW (President’s Proposal, effective for new beneficiaries beginning on January 1, 2027)

The President’s proposal would replace the current WEP calculation by implementing what the Greenspan Commission recommended: Determine a replacement rate based on the average covered and non-covered earnings, and then apply that replacement rate to the average earnings based solely on covered employment.

___________________________________________________________________________________________________________________________________________________________

Appendix C

Examples of Estimated Offset

Appendix C includes examples of how the proposed new computations could affect hypothetical benefit levels, including comparisons to benefit calculations under current law and under a potential repeal of WEP or GPO. As the examples show, some individuals could receive more benefits under the proposed new computations than they could expect under current law, while others could expect to receive less.

Our examples assume the following:

- Each of our six example couples has $46,500 in annual household earnings (between both spouses, and between covered and non-covered earnings).

- All beneficiaries have filed for retirement insurance benefits (and/or surviving spouse’s benefits) at full retirement age (no age reductions or delayed retirement credits apply). Pensions are assumed to be 67% of monthly average non-covered earnings.

- Under “New Calculation,” when discussing both the President’s proposal and Chairman Brady’s bill (H.R. 711), we presented the results as if both bills took effect in 2016. The effective date of the new calculations in the President’s proposal is 2027. The effective date for H.R. 711 is 2017.

- We have not included in the examples H.R. 711’s supplemental benefit for individuals whose benefits would be reduced due to current-law WEP.

- All estimated benefits are in 2016 dollars and use 2016 earnings assumptions.

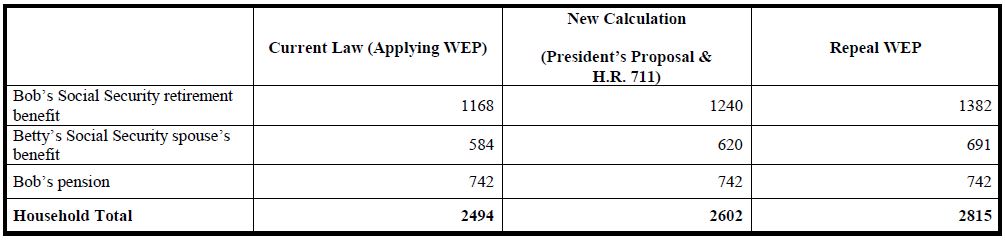

Windfall Elimination Provision

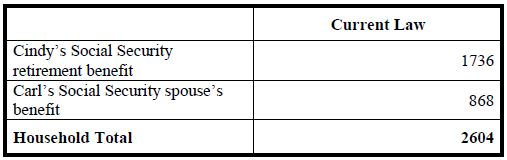

(Couple 1 and Couple 2 have identical earnings over 35 years.)

Couple 1

Bob has 25 years of covered earnings (avg. $46,500/yr.) and 10 years of non-covered earnings (avg. $46,500/yr.).

Bob receives a pension of $742/mo. based upon his non-covered earnings.

Betty, his spouse, had no earnings.

Couple 2

Cindy has 35 years of covered earnings (avg. $46,500/yr.) and no non-covered earnings.

Carl, her spouse, had no earnings.

Government Pension Offset

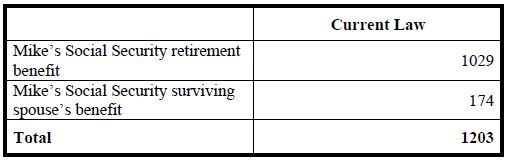

(Couple 3 and Couple 4 have identical earnings over 35 years.)

Couple 3

Abby has 35 yrs. non-covered earnings (avg. $20,000/yr.) without any covered earnings.

Abby receives a pension of $1,117/mo. based upon her non-covered earnings.

Her deceased spouse had 35 years of covered earnings (avg. $26,500/yr.) and no non-covered earnings.

Couple 4

Mike has 35 yrs. of covered earnings (avg. $20,000/yr.) without any non-covered earnings.

His deceased spouse had 35 years of covered earnings (avg. $26,500/yr.)

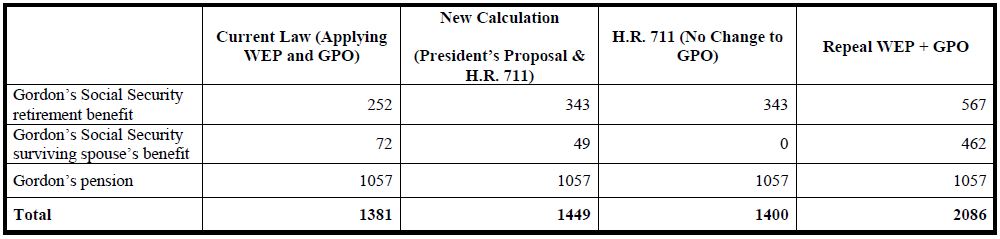

Windfall Elimination Provision and Government Pension Offset

(Couple 5 and Couple 6 have identical earnings over 35 years.)

Couple 5

Gordon has 10 yrs. covered earnings (avg. $26,500/yr.), and 25 yrs. non-covered earnings, (avg. $26,500/yr.).

Gordon receives a pension of $1,057/mo. based upon his non-covered earnings.

His deceased spouse had 35 years of covered earnings (avg. $20,000/yr.).

Couple 6

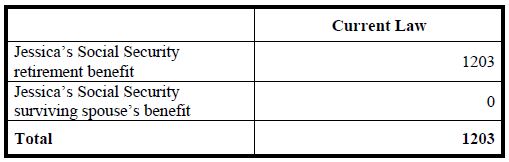

Jessica has 35 yrs. of covered earnings (avg. $26,500/yr.) without any non-covered earnings.

Her deceased spouse had 35 years of covered earnings (avg. $20,000/yr.).